On Wednesday this week, ServiceNow released its latest set of earnings results for Q1 2026. The results marked the latest stage in a long-running trend in ServiceNow earnings. While the company increased revenues and beat guidance for another successive quarter, its stock price has fallen sharply – by 15% at the time of writing.

As we reported at the time, the same phenomenon was seen after the last earnings report for Q4 2025, and again the quarter before. While much of this is down to the same trends, there’s a clear sense that the conflict in the Middle East weighed down on revenues, leading to a more muted earnings beat than might otherwise have been expected.

ServiceNow in Q1: A Modest Beat Masks Wider Concerns

Here are the headline figures from the latest ServiceNow earnings results:

- Subscription revenues in Q1 2026 were $3.67B. This represents 22% year-over-year growth, or 19% in constant currency. This is slightly higher than guidance from last quarter, which projected $3.65B, a year-over-year increase of 21.5%.

- Total revenue was $3.77B over the same period. This also represents 22% year-over-year growth, or 19% in constant currency.

- Remaining performance obligations (RPO) were $27.7B, representing 25% year-over-year growth, 23.5% in constant currency.1

- Current remaining performance obligations (cRPO) were $12.64B, representing 22.5% year-over-year growth, 21% in constant currency.2 This was in line with guidance from last quarter that projected 22.5% growth.

- Figure represents the total future revenue tied to existing contracts.

- Figure represents the portion of RPO that is due in the next 12 months.

Now, the company has once again updated its guidance for the remainder of 2026. Subscription revenues for 2026 are projected to be between $15.74B and $15.78B, a slight rise from last quarter’s figure of $15.53B-$15.57B.

In response, ServiceNow CEO Bill McDermott said, “ServiceNow’s first quarter performance beat the high end of our guidance, once again.”

Despite this, the extent of that beat is noticeably more muted than in recent quarters. Last quarter’s subscription revenue growth of $3.47B represented 21% year-over-year growth. This was 1.5% percentage points higher than the guidance issued after the Q3 2025 earnings release, of 19.5%. In contrast, this quarter’s subscription revenues figure (22%) was only 0.5 percentage points higher than last quarter’s guidance (21.5%).

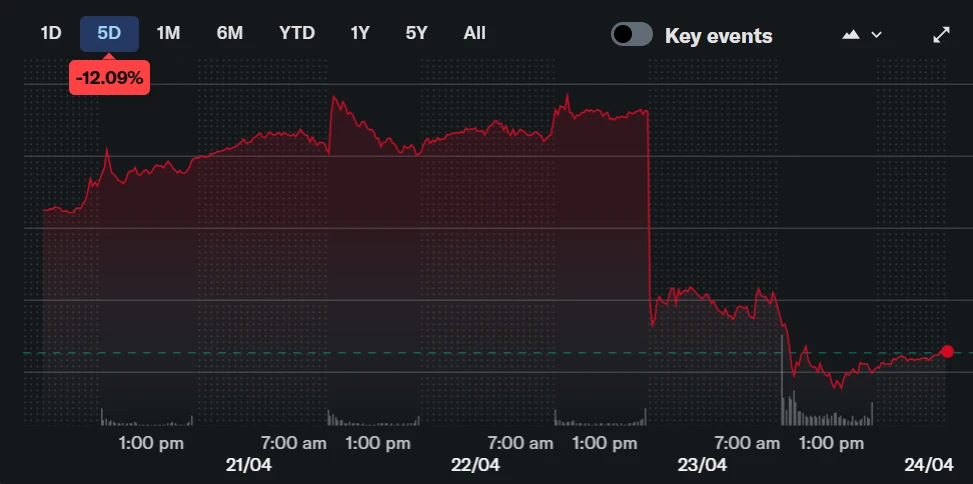

ServiceNow Stock Takes (Another) Nosedive

The financial results continue a trend we’ve reported on now for a few successive quarters: A guidance-beating earnings report, followed by an immediate drop in the company’s stock price.

On Tuesday this week (before the earnings call), ServiceNow’s stock (‘NOW’) was worth $100.14. By the close of trading yesterday, it had fallen to $84.78 – a drop of 15%. And this trend isn’t just restricted to earnings releases. Since the start of this year, the stock price has dropped by 43%, compared with its closing value on January 2, 2026 ($147.45).

In recent quarters, the sliding stock price has been attributed to a number of factors, including ServiceNow’s high price-to-earnings ratio, as well as wider concerns about the sustainability of the SaaS licensing model in the AI era.

To understand this phenomenon in more detail, we spoke to industry analyst Alecia Wall, Senior Enterprise AI Industry Analyst.

“The disconnect between ServiceNow’s operating performance and its stock price is striking to me,” she says.

“But there are real mechanical forces at work. NOW is overwhelmingly held by institutional investors who are navigating significant portfolio rebalancing right now – between geopolitical uncertainty, the broader SaaS repricing, and shifting AI narratives, fiduciaries are making hard choices about what to hold, and even strong performers get trimmed in that environment.”

“The disconnect between ServiceNow’s operating performance and its stock price is striking to me.”

Alecia Wall, Senior Enterprise AI Industry Analyst

In recent weeks, therefore, the stock price has been affected by a number of bearish revaluations, including one from UBS that we reported on last week. Then, UBS cut the stock’s rating from ‘buy’ to ‘neutral’ and reduced the price target from $170 to $100. This matches the trend from multiple other analysts. While many have maintained a ‘buy’ rating, the stock’s price target has been repeatedly revised down in recent weeks.

Is the Middle East Conflict Weighing on ServiceNow’s Stock?

The structural factors we discussed in the last section are still weighing down on ServiceNow’s stock price. But now, there’s another factor to add to the list: The conflict in the Middle East.

In the company’s quarterly live earnings call, McDermott said that the figures included “about a 75 basis point headwind from delayed closings of several large on-premise deals in the Middle East, due to the ongoing conflict in the region.”

This suggests that the revenue results and guidance raises would have been higher, had the conflict not occurred. Indeed, ServiceNow’s CFO, Gina Mastantuono, implied that its most recent guidance was deliberately conservative, as a result of this instability: “Our guidance captures that momentum, while taking a prudent view of the geopolitical environment, particularly the conflict in the Middle East, and its potential impact to deal timing.”

Much of the post-results coverage has focused on this. But according to Alecia Wall, the phenomenon is more down to timing than demand. “It’s a customer concentration dynamic, not a demand problem – and CFO Gina Mastantuono confirmed on the earnings call that a couple of those delayed deals have already closed in Q2.”

That being said, much still rests on how the situation develops in the next few weeks. “The harder question is what happens downstream,” Wall said.

“There’s a reasonable case for assuming a trend line of caution until proven otherwise, even though the underlying demand appears intact.” Therefore, she describes the updated guidance as “appropriately optimistic, without being irresponsibly positive.”

ServiceNow is keen to point out that the disruption didn’t stop the company from beating its guidance and posting strong results. As McDermott said on the call, “We’re not making any excuses. Our results are great. What we did explain is that there is a slight impact to the guide going forward in Q2, as a result of the war.”

Can ServiceNow Break Out of the Falling Stock Trend?

The curious thing about ServiceNow’s current stock price is this: Many analysts agree that the fundamentals for ServiceNow remain secure. The company has beaten guidance for successive quarters and continues to see impressive revenues in its growing portfolio of AI products.

Indeed, average deal sizes for the AI Control Tower more than doubled quarter-over-quarter in Q1, and Now Assist marked a 70% rise by the same metric.

These numbers point to a much more stable position for ServiceNow than its headline stock price would suggest. As Alecia Wall said, “The SaaSpocalypse narrative assumes that AI agents will erode ServiceNow’s value, but what I’m hearing from executives and platform leaders across the industry tells a very different story.”

Wall went on to suggest that ServiceNow was well-placed to act as a governance layer for AI. “The agentic wave is only as good as its governance,” she said. “Enterprises deploying AI agents at scale will need orchestration, observability, conflict resolution, and guardrails – and ServiceNow has spent years building exactly those control tower capabilities.”

“The agentic wave is only as good as its governance.”

Alecia Wall, Senior Enterprise AI Industry Analyst

This reading suggests that the stock is underpriced, and that ‘SaaSpocalypse’-related fears fail to understand ServiceNow’s unique value and business model. But given the stock’s rough ride over recent months, it seems that investors needed more than just a modest guidance beat to change their assessment.

With Knowledge 2026 just a few short weeks away, ServiceNow will be looking to move on from these headlines in short order. If last year’s announcements of the AI Control Tower and AI Agent Fabric are anything to go by, the company will be hoping to cement its credentials as an AI enabler. Whether investors will agree very much remains to be seen.