ServiceNow has announced its financial results for both Q4 2025 and the full year 2025. Like recent quarters, the results were consistently positive, with financial forecasts (‘guidance’) being exceeded across all major metrics. The figures also suggested continuing momentum and adoption of ServiceNow AI products, such as Now Assist.

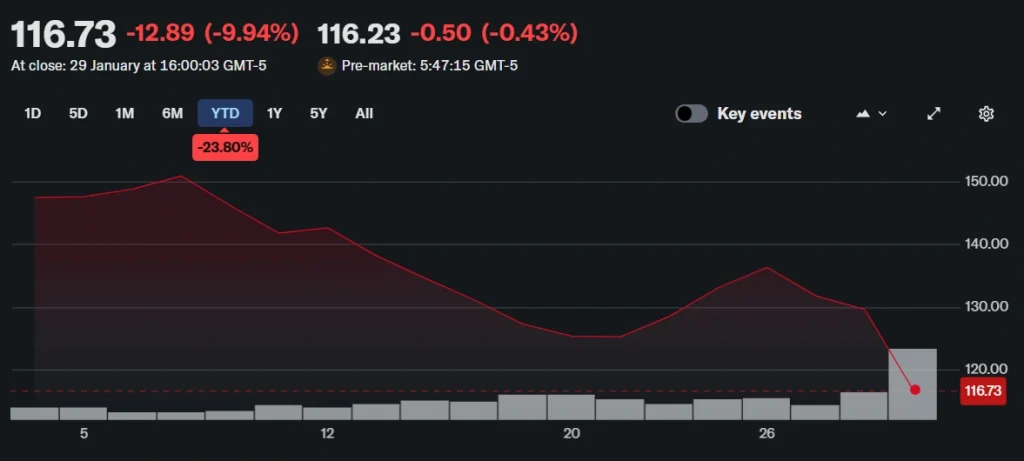

Despite this, ServiceNow’s stock has continued to decline in recent days, having fallen from $147.45 at the start of the year to $129.62 on Wednesday, and further to $116.73 by the end of Thursday. This also continues the trend we discussed in previous quarters.

ServiceNow Exceeds Guidance on All Topline Metrics in Q4 2025

Here are the main financial figures for Q4:

- Subscription revenues hit $3.46B in Q4 2025. This represents 21% year-over-year growth vs. the same figure in Q4 2024 (19.5% in constant currency). The figure is also up from both Q3 ($3.29B) and Q2 ($3.11B), respectively.

- Total revenue in Q4 2025 was $3.57B. This shows 20.5% year-over-year growth (19.5% in constant currency). This is an increase from Q3 ($3.4B) and Q2 ($3.22B).

- Remaining performance obligations (RPO) were $28.2B as of Q4 2025, a particularly sharp year-over-year increase of 26.5% (22.5% in constant currency).¹

- Current remaining performance obligations (cRPO) were $12.85B, representing 21% year-over-year growth (constant currency).²

- Now Assist, the company’s flagship AI product, has also exceeded expectations, surpassing $600M in annual contract value (ACV). This has more than doubled year-over-year.

¹ – Figure represents the total future revenue tied to existing contracts.

² – Figure represents the portion of RPO that is due in the next 12 months.

Unsurprisingly, ServiceNow is keen to highlight the continued success that these financial figures demonstrate. Bill McDermott, ServiceNow’s CEO, said: “ServiceNow significantly beat Q4 expectations, accelerated net new business, and issued exceptional guidance for 2026. We had substantial growth in licensed users, workflows, and transactions on our platform.”

The company also highlighted how its AI investments have contributed to these impressive results. “Q4 was another strong quarter, concluding a remarkable year of AI innovation, with emerging products like Now Assist, Workflow Data Fabric, Raptor, and CPQ all outperforming,” said ServiceNow President and CFO, Gina Mastantuono.

2025 in Summary: How Did ServiceNow Perform Last Year?

ServiceNow also released highlights for 2025’s full-year financial figures:

- Subscription revenues were $12.88B, representing a 20.5% year-over-year growth*.

- Remaining performance obligations grew by 22.5% year-over-year* and current remaining performance obligations were 21% year-over-year*.

* All figures are reported in constant currency

Off the back of these figures, guidance for 2026 has been updated. The company now expects subscription revenues in 2026 to be between $15.53-$15.57B. This would represent an increase of around 20%. According to MSN, this is somewhat higher than analyst expectations of around 18.5%.

Again, these figures demonstrate consistent success and adoption of the ServiceNow platform.

So, What’s Going On With NOW Stock?

The last few quarters have shown a curious phenomenon: ServiceNow’s stock (‘NOW’) has consistently dropped, despite successive quarters of impressive results.

At the time of writing, it seems this trend is being repeated in the aftermath of the Q4 earnings results. In the 24 hours after the financial figures were released, the stock fell by almost 10%, from $129.62 at the end of Wednesday to $116.73 on Thursday.

In total, this is down about 20% compared with the start of the year, when the closing value on January 2, 2026, was $147.45.

So, what’s going on? And why does this keep happening?

It’s important to note that this phenomenon isn’t restricted to ServiceNow; other SaaS companies like Adobe and Salesforce have seen a similar performance in recent months. Much of this is down to AI, with investors worrying that traditional software functionality is becoming increasingly redundant in the AI era. At the same time, there are concerns that widespread AI-related redundancies could undermine the SaaS industry’s seat-based pricing model.

ServiceNow CEO Bill McDermott hinted at these concerns in a recent interview, saying: “We don’t live in the SaaS neighborhood. Functional SaaS and feature SaaS will be automated by ServiceNow and the language models that are meeting us in the middle of our workflow, where business happens.” Clearly, the company is keen to point out that it’s not like other SaaS companies.

But for ServiceNow, there are more specific and technical challenges. Crucially, some investors worry that the company’s high price-to-earnings ratio (Trailing: 69.90, Forward: 28.33) signals that the stock is overvalued. This is more than twice the value of Salesforce, for instance. Additionally, the updated 2026 subscription revenue guidance (indicating around 20% growth) was viewed as optimistic by some investors who’d been expecting a lower figure of around 18%. This implies the guidance is on the more optimistic side, suggesting the chances of it being beaten again this year are lower.

Elsewhere, ServiceNow’s ambitious recent acquisition strategy is also a running sore for the company’s stock. Over the last year, it has announced its three most expensive acquisitions of all time: Moveworks ($2.85B), Veeza (rumored to be $1B+), and Armis (a staggering $7.75B).

You only need to look at the stock performance since the start of December (before Veeza and Armis were announced) to see this result in action: The closing value on December 1, 2025, was $164.41. Indeed, concern around ServiceNow’s acquisitions is so pronounced that it was referenced directly by Bill McDermott in the investor earnings call on Wednesday:

“We did not and never have bought an asset like many others have… because we needed the revenue. What we needed [was] the innovation and the expanded growth opportunity.” McDermott went on to suggest a quieter period for ServiceNow acquisitions might yet be ahead, saying: “And no, we’re not going after anything large. We now have them in the family and we’re going to grow them like we do everything else.”

Given these comments and ServiceNow’s volatile stock movements, there’s a good chance the ServiceNow acquisition scene will be notably quieter in the near future.

ServiceNow Announces $5B Share Repurchase Program

Alongside its Q4 earnings release, ServiceNow also took the opportunity to announce several other updates. Most notably, this included a $5B Share Repurchase Program, with $2B of that intended to be ‘imminent’. The decision is designed to manage the impact of share dilution, which describes when a company releases additional shares, reducing the ownership percentage of each individual shareholder. The move is therefore designed to reverse this phenomenon.

As well as this, several partnerships and strategic collaborations were also announced:

- A new strategic partnership with Anthropic, intended to better integrate Claude AI models into the ServiceNow AI platform.

- A strategic commitment with Finserv, a fintech and global payments company, which will scale its use of ServiceNow products (Now Assist, Financial Services Operations (FSO), and IT Service Management (ITSM)) to improve its operations.

- Panasonic Avionics Corporation has also expanded its relationship with ServiceNow, aiming to replace ‘legacy systems’ with the ServiceNow CRM and Now Assist.

A Mixed Start to 2026?

While the financial results and strategic partnerships are clearly good news for the company, there is clearly ongoing concern around NOW stock’s performance in recent weeks and months. Given the ongoing discussions around a potential ‘AI bubble’ correction, analysts will be keeping a close eye on the performance of NOW and its software peers over the coming weeks and months.

Despite this, the fundamentals for ServiceNow are clearly robust. As the year progresses, the chances of further impressive financial results are good.